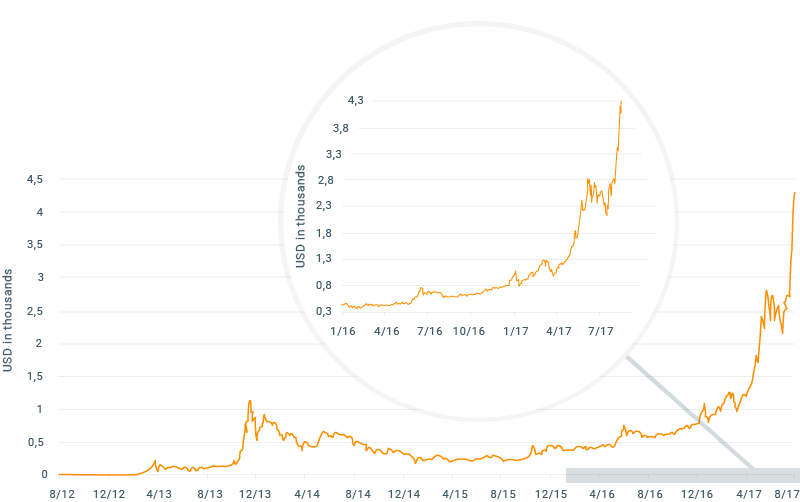

Please be aware that the presented data is only a prediction and such is not a reliable indicator of future performance.

In this simulation, the cost of transaction using Bitcoins reaches the current cost of the banking system only by 2032 but it’s worth bearing in mind that the banking system will adjust over time and could offer much more competitive fees today. Would that suggest that a current Bitcoin price is too high and/or assumption of 10% annual price increase is too optimistic? We will leave it for readers to conclude. One needs to keep in mind that when we change assumptions about amount of transactions in block we can obtain different results. Furthermore, Bitcoin has more features than just cost. It is also has a time of confirmation that at present is much shorter than in banking system as well as the privacy trait that is valuable for many (including shadow economy). On the other hand, it might be the case that rival technologies (including blockchain ones) will capture market share from Bitcoin offering cheaper and more efficient services. Therefore this simulation is only for demonstrative purposes. In the next section we present some interesting third party views on Bitcoin price.

Section 3

Bitcoin theories and predictions

In the previous section we presented one way of looking at Bitcoin valuations. However with cryptocurrencies being so new on the market and their price action explosive, there are many views, some of which are radically different. Many opinions include merely price targets without details or valuation methods. In this section we present selected views, in which some from of valuation-based approach has been present.

Ronnie Moas - $7,500 in 2018

Ronnie Moas is a respected equity analyst in the United States and claims to be ranked #9 stock picker between 2008 and 2017 in a group of 4,558. His approach is to compare Bitcoin to the Internet in the 90s and treat cryptocurrencies as an investable asset class. His original forecast of $5000 price in 2018 was based on the fact that a capitalisation of cryptocurrencies was just at 1/25 percent of global capitalisation of stocks, bonds, gold and cash. Moas is sure that when these currencies are established as an investable asset class, this share will increase to at least 2 percent and currency prices will be 100 times higher. Moas changed his forecast to $7500 in 2018 after Bitcoin price broke the $4000 barrier. Do notice that there is no mathematical formula between a share of cryptocurrencies in an array of investable assets and the price of Bitcoin and therefore the price target is Moas’ guess in this case.

Tom Lee, Fundstrat Global Advisors - at least $20,000 by 2022

Tom Lee, ex-chief equity strategist at JP Morgan, is the first renowned Wall Street strategist to issue a forecast on Bitcoin price. He constructed a model that assumes a growing substitution from gold into Bitcoin. He noted that market capitalisation of gold was above $7.5 trillion, 130 times above Bitcoin’s. He sees investors treating Bitcoin as a store of value and central banks starting buying cryptocurrencies when their market capitalization exceeds $500 billion, providing legitimacy of those currencies and inviting additional demand from investors.

Kay-Van Petersen, Saxo Bank - $100,000 in 2027

Petersen’s forecast is among the most bullish of all as it assumes annual rate of return of nearly 40% for the next ten years even at the current Bitcoin price. Petersen thinks that cryptocurrencies will capture 10% of the total currency trading volume (over $5 trillion daily) within a decade and Bitcoin could enjoy a third of this pie. He notes that a daily traded volume is typically about 10% of capitalisation in the case of Bitcoin and that would take its cap to $1.75 trillion. Keep in mind that Petersen did not lay out assumptions indicating why cryptocurrencies would reach that level of trading so again one needs to be careful with this kind of valuation.

Jeremy Liew, Peter Smith - $500,000 by 2030

If Petersen’s view isn’t bullish enough Jeremy Liew, the first Snapchat investor and Peter Smith, CEO of Blockchain have an even bolder one. They see Bitcoin prices at $500,000 by 2030 and even provide a calculation behind this forecast. They assume that network users will grow by a factor of 61 until 2030 to reach 400 million. They see a popularisation on Bitcoin-based remittances and mobile penetration supporting this tendency. Moreover, they assume that each user would hold Bitcoins worth $25,000 and thus arrive at a market cap of $10 trillion. With a supply of around 20 million that would leave the price at $500,000. Obviously a number of users and their average Bitcoin holdings are huge question marks in this calculation.

BitVal model - below $2,200

Many opinions and theories on Bitcoin prices lack discipline that is required by valuation modelling. The Financial Times presented an approach of an analyst who chose to stay anonymous and constructed a BitVal model where Bitcoin price is linked to a percentage of money laundering in the global GDP. BitVal assumes that a relationship between the price of Bitcoin and the extent of global money laundering should be stable in a longer run because Bitcoin is often used to transfer money without regulatory oversight. The model uses data between January 2014 and May 2017 and even at a price of $2,200 finds the cryptocurrency to be grossly overvalued. However, one could question a chosen range of the data as Bitcoin has become far more popular since January 2014. Even if the BitVal estimate could be questioned it shows that some observers perceive Bitcoin’s utility as a means of transferring money outside of governments’ control.

Please be aware that ideas presented above are third party predictions and as such are not a reliable indicator of future performance. XTB will not accept liability for any loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

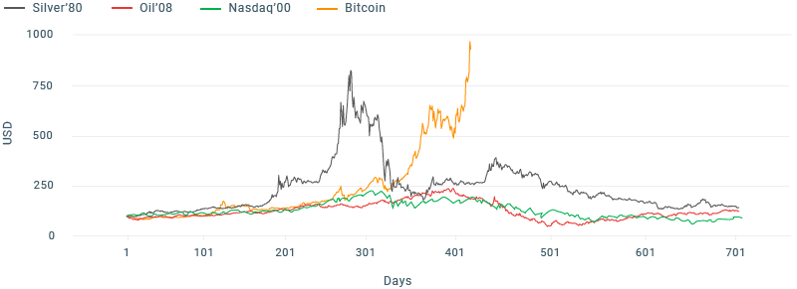

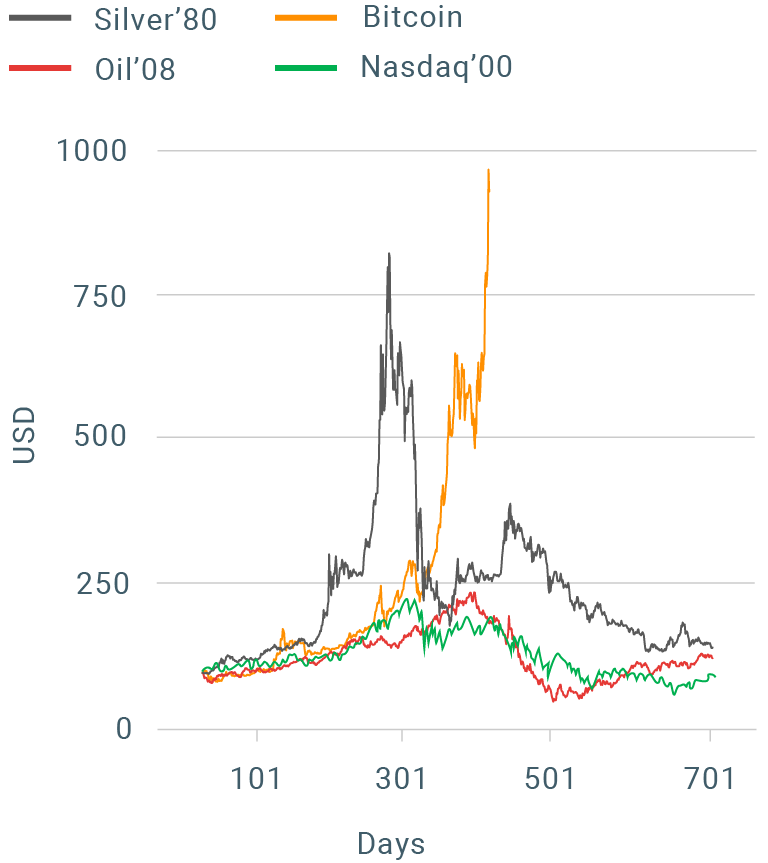

Seeing a giant rally in Bitcoin price so far, one could ask if this is already a bubble?

Section 4

Is Bitcoin in a bubble?

Speculative bubbles are not new to financial markets. From tulip hysteria, through South Sea Company, through British railway mania and the most recent dot.com bubble, investors from many generations witnessed an euphoria of a boom and a panic of a crash. Is Bitcoin next in line?

First, we compare Bitcoin price development with silver, oil and Nasdaq Composite from periods when these markets experienced a massive surge in price followed by a crash. We chose relatively recent bubbles because of data availability (unfortunately there is no daily time series on Tulip prices from the 17th century) and selected the silver peak in 1980, the Nasdaq Composite that reached a high in 2000 and oil from the “peak oil” period that culminated in 2008.

Because timelines of these price developments differ, we simply choose the 1st of January of a year preceding a crash for a starting point. One thing is common for all these markets including Bitcoin: there’s a period when price increases are relatively modest which is followed by a rapid price explosion. Similarities end at this point, though. We can see that oil and the Nasdaq look very benign in comparison to silver and Bitcoin. This is partly because these markets were on the rise for years heading into the crash. While the boom and bust of the silver market in 1980 was far more dynamic, it still pales in comparison to recent developments in the Bitcoin price.